New Delhi, June 2026 – India’s smartphone market, one of the world’s largest, continues to evolve rapidly even as it faces headwinds in early 2026. According to recent data from IDC, Counterpoint Research, and other trackers, shipments declined in Q1 2026 (down ~3-5% YoY to around 31 million units), marking one of the weakest quarters in recent years. However, the market’s value grew due to rising average selling prices (ASP reaching a record ~US$302) and a clear shift toward premium and mid-range devices.

Market Overview and Key Trends

- Volume vs. Value: While unit shipments dipped due to memory price inflation, post-festive slowdown, and cautious consumer spending, the market is transitioning from volume-driven to value-driven growth. Offline channels strengthened their dominance (around 62% share).

- Long-term Outlook: The market is projected to grow at a CAGR of ~6.5% from 2026-2034, reaching nearly 296 million units by 2034, fueled by 5G adoption, digitalization, and improving affordability in lower segments over time.

- Challenges: Rising component costs (especially memory, up significantly), rupee depreciation, and extended replacement cycles are pressuring entry-level demand. Brands front-loaded inventory in Q1 to counter expected price hikes.

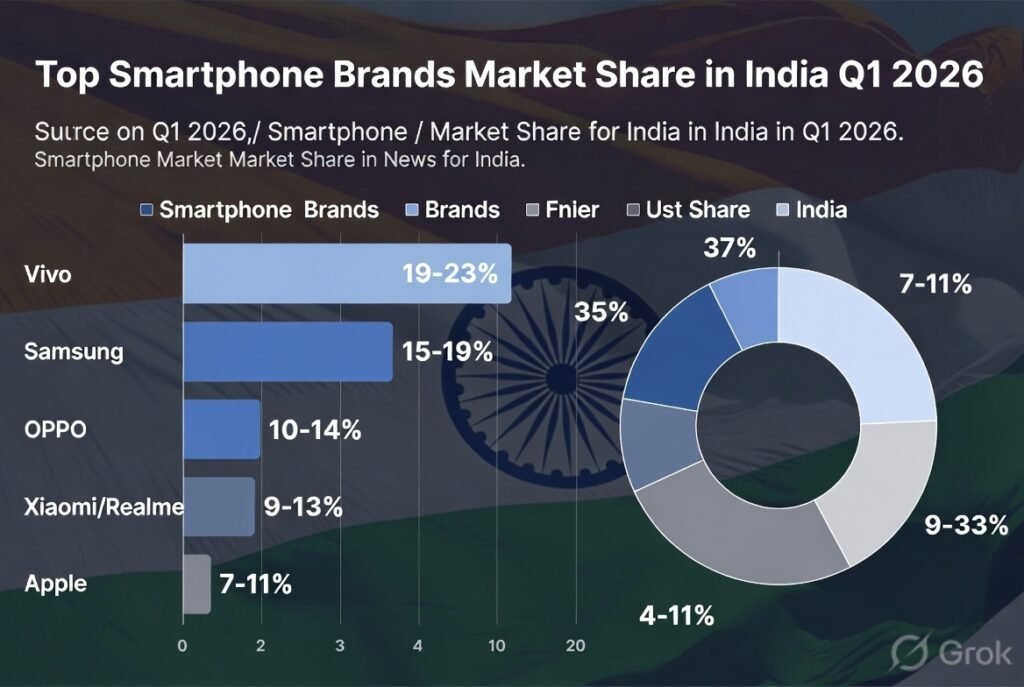

Top Smartphone Brands in India (Q1 2026 Snapshot)

Vivo has solidified its position as the market leader, benefiting from a strong mid-range portfolio, aggressive marketing, and value offerings. Samsung has shown resilience with premium pushes, while Chinese brands continue to dominate the mid-to-budget segments. Apple is making notable gains in the premium space.

Approximate Market Shares (Q1 2026, compiled from multiple trackers):

- Vivo (incl. iQOO in some reports): ~19-23% – Leader with strong traction in mid-range and entry-premium.

- Samsung: ~15-17% – Strong No. 2, boosted by Galaxy series and A-series popularity.

- OPPO (excl. Realme/OnePlus in some data): ~15-17% – Solid growth in budget and mid-range.

- Xiaomi / POCO / Realme: Combined strong presence (~10-15% each or grouped) – Focus on affordable 5G and performance devices.

- Apple: Growing to ~9%+ in shipments, record performance in premium with iPhone 16/17 series momentum.

- Others: Motorola gaining ground, alongside smaller players.

- Segment Performance

- Entry-Level (<US$100): Strong growth (~35% YoY in some quarters), led by Xiaomi, Realme, and Vivo.

- Mass-Budget (US$100-200): Dominated by Vivo, OPPO, Realme.

- Entry-Premium (US$200-400): Vivo, OPPO, Samsung, and Motorola leading.

- Premium: Apple and Samsung excel here, with AI features, better cameras, and displays driving upgrades.

Qualcomm-powered devices gained share, while MediaTek remains significant.

Key Drivers and Future Outlook

- 5G and AI Integration: Brands are pushing AI features, better cameras, and gaming performance to justify higher prices.

- Manufacturing Push: India’s PLI scheme continues to attract investment, boosting local production and exports.

- Consumer Behavior: Urban consumers favor premium devices; rural and budget segments remain price-sensitive amid economic pressures.

- 2026 Forecast: Analysts expect continued pressure in the first half, with potential recovery later in the year driven by festive seasons and new launches. Double-digit declines are possible in some quarters if costs remain high.

The Indian smartphone market remains highly competitive and dynamic, with Chinese brands (Vivo, OPPO, Xiaomi ecosystem) holding the bulk of volume share, while Samsung and Apple lead in brand prestige and premium revenue.

Sources: Data aggregated from IDC, Counterpoint Research, Omdia, Statcounter, and industry reports (as of mid-2026). Market shares are approximate and can vary slightly by methodology and exact quarter.

This report provides an overview based on the latest available industry data. For the most current figures, refer to quarterly tracker reports.